How Much Mortgage Can I Afford?

by Editorial Staff 4:42 pm

Mortgage

How Much Mortgage Can I Afford? A Comprehensive Guide to Homeownership

Buying a home is one of the most significant financial decisions you will make in your lifetime. With home prices soaring in many regions and interest rates fluctuating, understanding how much mortgage you can afford is crucial before diving into the house-hunting process.

If you take on too large a mortgage, you could find yourself financially stretched, while a smaller mortgage may limit your options.

This article aims to guide you through the key factors that determine how much mortgage you can afford, strategies to help you secure the best deal, and what to do if you can’t afford the mortgage you initially had in mind.

Whether you’re a first-time buyer or you’re returning to the market, this guide will provide you with the knowledge to make a smart, informed decision.

Understanding How Much Mortgage You Can Afford

Before you begin shopping for homes, it’s essential to have a clear understanding of how much you can afford.

There’s no universal answer, as your mortgage affordability will depend on a variety of factors such as income, debt, credit score, and down payment amount.

While there are various online tools to give you an estimate, the reality is often more nuanced.

In this section, we’ll break down these factors in detail, explore how lenders assess your eligibility, and provide practical tips to ensure you’re financially ready for a mortgage.

1. Income: The Foundation of Your Borrowing Capacity

Your income plays the most crucial role in determining how much mortgage you can afford. The amount you earn will set the upper limit of what a lender is willing to offer you.

Lenders typically evaluate your gross monthly income—that is, the total amount you earn before taxes, benefits, and deductions.

This figure forms the basis of your monthly mortgage payments, and it helps lenders calculate the amount they’re comfortable lending to you.

However, it’s important to note that lenders are not just concerned with your base salary. Additional sources of income such as bonuses, overtime, alimony, child support, or rental income can also be factored in, provided you can demonstrate a consistent and reliable track record of these earnings.

For example, if your base salary is $60,000 a year ($5,000 per month), but you earn an additional $1,000 per month from freelance work, your total monthly income for mortgage calculation purposes would be $6,000. This could allow you to borrow more, assuming other factors are favorable.

Example:

- Gross annual income: $60,000

- Additional income: $12,000 from side gig

- Total income for mortgage calculation: $72,000 ($6,000/month)

Lenders may also factor in the stability of your income. Someone who has been employed in the same job for several years is seen as a lower risk compared to someone who has just started a new job or is self-employed.

If your income is variable or seasonal, it’s important to demonstrate your average earnings over time.

2. Debt-to-Income Ratio (DTI): How Much Debt Is Too Much?

The Debt-to-Income ratio (DTI) is a critical measure lenders use to assess your ability to take on additional debt.

Your DTI ratio compares your monthly debt payments to your gross monthly income. This includes not just the mortgage you’re applying for, but also any other debts you may have, such as car loans, student loans, credit card debt, or personal loans.

Lenders use your DTI ratio to determine how much additional debt you can handle without overstretching your finances.

A high DTI ratio can make you a riskier borrower, potentially leading to a higher interest rate or a denied loan application.

Lenders typically prefer a DTI ratio of 43% or less. However, certain loan types or government programs (such as FHA loans) may allow for higher DTI ratios, especially if you have a strong credit score or a large down payment.

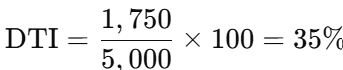

How to Calculate DTI:

To calculate your DTI, add up all your monthly debt payments, including your expected mortgage payment. Then divide the total by your gross monthly income and multiply by 100 to get a percentage.

Example:

- Monthly debt payments:

- Mortgage: $1,200

- Car loan: $300

- Student loan: $150

- Credit card payment: $100

- Total monthly debts = $1,750

- Gross monthly income = $5,000

In this example, a DTI ratio of 35% would generally be considered favorable by most lenders.

3. Credit Score: Your Financial Reputation

Your credit score is another key factor that influences both your mortgage eligibility and the interest rate you’ll be offered.

The higher your credit score, the lower the risk you are to lenders, and therefore the more favorable your mortgage terms will be.

Most lenders require a minimum credit score of 620 for conventional loans, but for the best rates, a score of 740 or above is often needed.

If your credit score is lower than this, you may still qualify for a mortgage, but you’ll likely face higher interest rates, which means higher monthly payments and more paid in interest over the life of the loan.

FICO Score Ranges:

- Excellent (740-850): Best mortgage rates

- Good (670-739): Fairly competitive rates

- Fair (580-669): May qualify for FHA or subprime loans with higher rates

- Poor (300-579): Likely to face higher rates or difficulty qualifying

Your credit score is derived from factors like:

- Payment history (35%): Late payments, bankruptcies, or defaults can significantly lower your score.

- Credit utilization (30%): The ratio of your credit card balances to your credit limits. It’s best to keep this below 30%.

- Length of credit history (15%): A longer credit history can improve your score.

- Credit mix (10%): A diverse range of credit accounts (credit cards, auto loans, mortgages) can boost your score.

- Recent inquiries (10%): Too many recent credit inquiries can negatively impact your score.

Improving your credit score, even by a few points, could result in a significantly better mortgage rate. You can improve your score by paying off outstanding debt, making timely payments, and reducing credit card balances.

4. Down Payment: The Larger the Down Payment, the Lower the Loan Amount

The down payment is one of the first things a lender will consider. A larger down payment reduces the amount you need to borrow, thereby lowering your monthly mortgage payments and your overall interest payments.

A typical down payment for a conventional loan is 20% of the home’s purchase price. However, depending on the type of loan, you may be able to put down less.

For example:

- Conventional Loans: Typically require a down payment of 20%. However, some lenders offer options with as little as 3% down for first-time homebuyers.

- FHA Loans: Require as little as 3.5% down.

- VA Loans: Available to eligible veterans and active military, often requiring no down payment.

- USDA Loans: Offer 0% down payment options for homes in rural areas.

It’s important to note that putting down less than 20% typically means you’ll have to pay for private mortgage insurance (PMI), which protects the lender if you default on the loan.

This increases your monthly mortgage payment, so a larger down payment can save you money in the long run.

Example:

- Home price: $300,000

- 20% down payment: $60,000

- Loan amount: $240,000

- Monthly mortgage payment will be lower compared to a 3% down payment loan, where the loan amount is $291,000.

A larger down payment also signals to lenders that you’re financially stable and less risky, potentially helping you secure better loan terms.

5. Interest Rates: The Cost of Borrowing

The interest rate is one of the most important elements of your mortgage. It directly influences your monthly payments and the total cost of your loan.

Even a small difference in interest rates can have a significant impact over the life of your mortgage.

Interest rates are affected by various factors, including:

- Economic conditions: Rates fluctuate based on inflation, economic growth, and the policies of central banks like the Federal Reserve.

- Your credit score: The higher your credit score, the better the rate you’ll receive.

- Loan type and term: Fixed-rate loans tend to have higher rates than adjustable-rate mortgages (ARMs), but offer the stability of consistent payments.

- Down payment: A larger down payment may result in a better interest rate.

Example:

Consider the impact of a 1% difference in interest rates:

- Loan amount: $250,000

- 30-year loan term

- Interest rate 3%: Monthly payment = $1,054

- Interest rate 4%: Monthly payment = $1,193

A difference of just 1% in interest rate results in a $139 higher monthly payment. Over the course of the loan, that could mean tens of thousands of dollars in additional payments.

Tips for Securing the Best Mortgage Rate

Securing the best mortgage rate is crucial for keeping your home affordable. Here are some strategies to help you lock

in the best deal:

- Improve Your Credit Score: The higher your credit score, the better your mortgage rate. Pay bills on time, reduce your credit card balances, and avoid opening new credit accounts.

- Shop Around for Lenders: Mortgage rates can vary from lender to lender. Don’t settle for the first quote you receive. Compare rates and fees from multiple lenders to find the best deal.

- Consider a Shorter Loan Term: If you can afford higher monthly payments, a 15-year mortgage will typically come with a lower interest rate than a 30-year loan. You’ll pay less in interest over the life of the loan.

- Get Pre-Approved: Pre-approval gives you a clear idea of how much mortgage you can afford and demonstrates to sellers that you’re a serious buyer. It also locks in an interest rate, which can be helpful if rates are rising.

- Consider Paying Points: Mortgage points are upfront fees you can pay to lower your interest rate. Each point typically costs 1% of the loan amount and can reduce your rate by about 0.25%. This could be worth considering if you plan to stay in your home for the long term.

What to Do If You Can’t Afford the Mortgage You Want

If, after calculating all these factors, you realize that the mortgage you desire is out of reach, don’t panic. There are several things you can do to improve your financial situation:

- Increase Your Income: Look for ways to increase your income, such as taking on a second job, asking for a raise, or starting a side business.

- Reduce Your Debt: Lower your debt-to-income ratio by paying down existing debt, such as credit card balances, car loans, or student loans.

- Save for a Larger Down Payment: If possible, save more for your down payment. A larger down payment will reduce your loan amount and help lower your monthly payments.

- Consider a Less Expensive Home: If you can’t afford the home you want, consider looking for a more affordable property or exploring different locations where prices are lower.

- Consider Government Programs: Look into FHA loans, VA loans, or USDA loans if you meet the eligibility criteria. These programs offer lower down payments and more flexible terms.

Final Thoughts

Determining how much mortgage you can afford involves more than just looking at your income—it requires an assessment of your debt, credit score, and savings for a down payment.

While the process may seem complex, understanding these factors and how they work together can help you make an informed, realistic decision about your home purchase.

By improving your financial health, shopping around for the best mortgage rates, and considering government-backed loan programs, you can secure a mortgage that fits within your budget.

Taking the time to plan ahead will help ensure that your mortgage payments remain manageable and that you can enjoy your new home without financial stress.

Remember, the key to successful homeownership is finding a balance between your dream home and what you can afford.

With careful preparation, smart decisions, and a clear understanding of your finances, homeownership can be an exciting and rewarding experience.